Contract leakage in procurement: how to verify that your negotiated conditions are properly applied

Contract leakage refers to the gap between what has been negotiated and what is actually paid.

This contract leakage can be caused by a forgotten discount on an invoice, a price updated on the supplier's side but not in your system, a unit price slightly higher than that on the purchase order.

Individually, each discrepancy seems negligible. Cumulated over a month, over a year, and across all suppliers, they represent a direct and silent margin loss.

What makes contract leakage particularly insidious is that it is invisible in your usual reports. The ERP records what has been entered and paid, not what should have been.

Result: you think you have the situation under control, while margin points are slipping away at every billing cycle.

This article explains where contract leakage comes from, what control checkpoints to put in place on each procurement document, and how to move from occasional control to systematic control that durably protects your margins.

Understanding contract leakage: where does it come from?

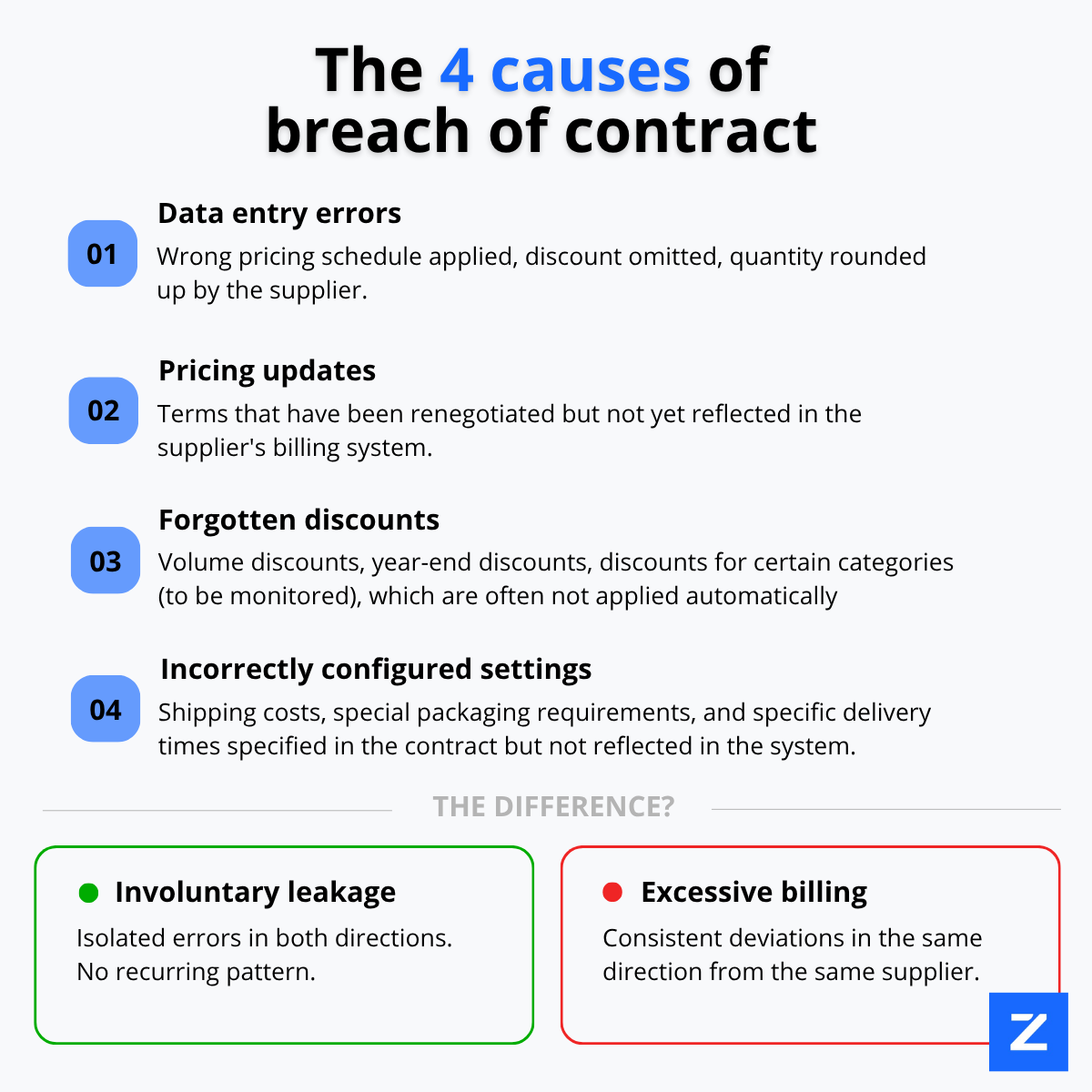

The first thing to understand about contract leakage is that it is rarely intentional. In the vast majority of cases, it results from human errors, synchronisation failures between systems, or poorly configured contractual conditions, and not from a deliberate intent to overbill.

The most frequent origins are as follows:

Data entry errors on the supplier side: a data entry operator who applies the wrong pricing scale, a forgotten discount line, a quantity rounded upwards. These errors are frequent in organisations where invoicing is still largely manual or semi-automated.

Pricing updates not passed on: conditions were renegotiated at the start of the year. But on the supplier side, the invoicing department was not informed in time or their system was not updated. Result: the old pricing scales apply for weeks, sometimes months.

Forgotten or incorrectly applied discounts: volume discounts, year-end discounts, category discounts. These negotiated conditions are often complex to manage. They require active monitoring of thresholds and application periods that many suppliers do not manage in an automated way.

Specific conditions poorly configured: free shipping above a certain order amount, specific packaging, particular payment terms. These conditions appear in the contract, but they are not always correctly translated into the supplier's management systems.

Involuntary leakage vs abusive invoicing: knowing how to tell the difference

There is however a second category, less comfortable to address: abusive invoicing. This refers to cases where a supplier knowingly invoices conditions that do not match those negotiated, betting on the fact that you do not systematically control.

In practice, the line between repeated error and deliberate practice is not always easy to draw. What makes it possible to distinguish them is the frequency and directionality of the discrepancies: if the errors systematically go in the same direction (always in favour of the supplier, never in your favour), they deserve particular attention.

The order of magnitude to keep in mind

Depending on sectors and procurement volumes, contract leakage represents on average between 1% and 5% of total procurement spend. On a procurement budget of 5 million euros, that represents between €50,000 and €250,000 in lost margin every year without anyone in the organisation truly being aware of it.

The control checkpoints to put in place on each procurement document

Controlling contract leakage cannot be improvised. It is based on a simple principle: at each stage of the procurement cycle, a document must be cross-referenced with the previous one and with the reference contractual conditions. Here is how to proceed concretely.

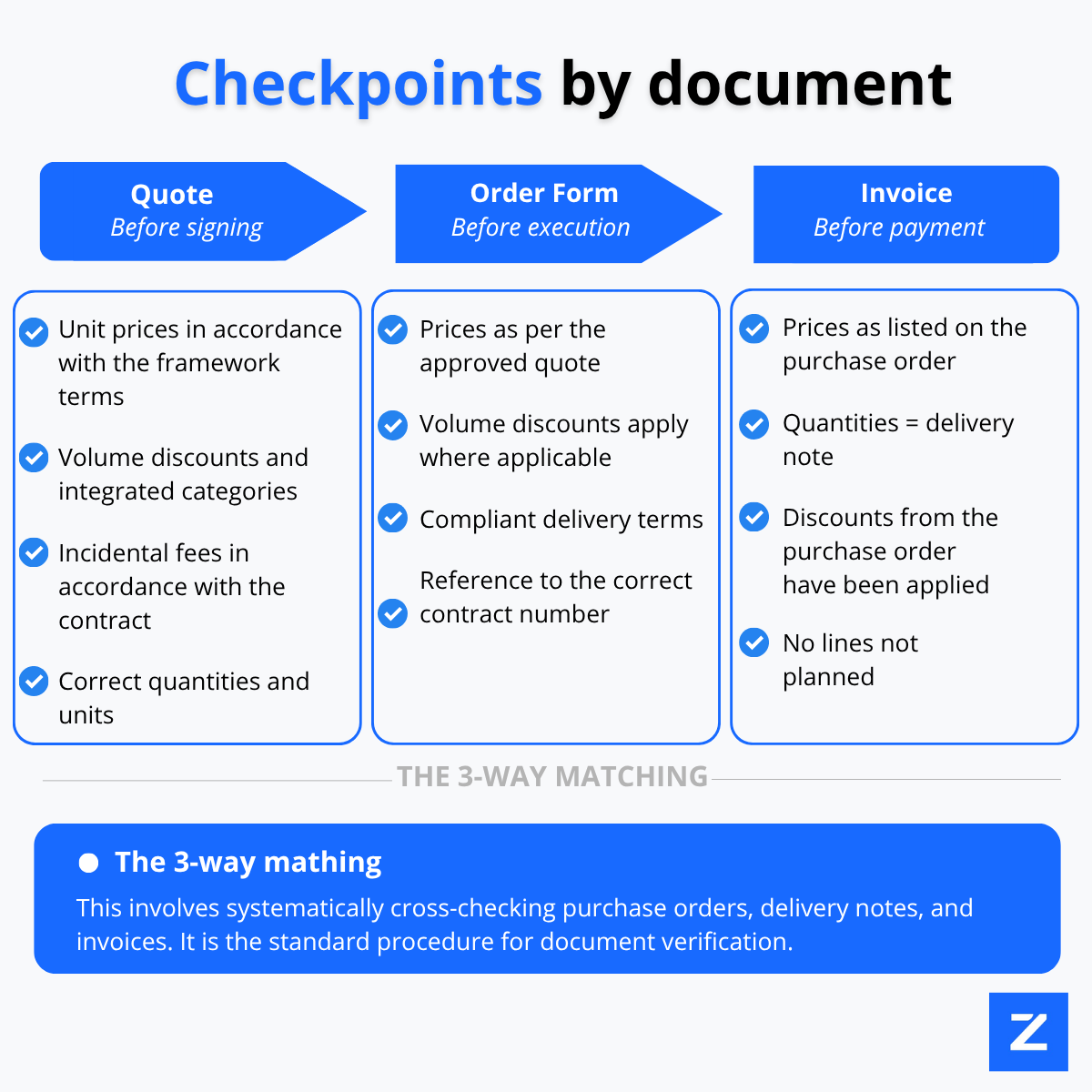

On the quote: verifying consistency before any commitment

The quote is the first control checkpoint and it is where it is easiest and least costly to intervene, because no financial commitment has yet been made.

What to check on each quote:

Do the unit prices correspond to the negotiated framework conditions or the last validated pricing scale?

Are the discounts applicable to this order (volume discount, category discount) properly included?

Are the ancillary costs (transport, packaging, commissioning fees) in line with what was contractually agreed?

Do the quantities and units of measurement correspond to what was requested?

A quote not controlled before validation becomes a problematic purchase order, then a disputed invoice. Correcting it at this stage takes a few minutes. Correcting it after invoicing takes several days.

On the purchase order: the last safety net before commitment

The purchase order materialises your commitment. It must be the exact transcription of what was negotiated, not an approximate manual entry.

What to check on each purchase order:

Do the unit prices entered correspond to the validated quote and the contractual conditions?

Do the quantities ordered trigger a volume discount? If so, is it correctly indicated?

Are the delivery conditions (lead times, incoterms, shipping costs) in line with the contract?

Does the purchase order reference the correct contract or framework agreement number?

This control checkpoint is often overlooked because it requires cross-referencing several sources of information at the same time: the contract, the quote, the pricing history. It is precisely this complexity that makes it difficult to carry out manually at scale.

On the invoice: the final and most critical control checkpoint

The invoice is the document on which contract leakage materialises financially. It is here that the gap between what was negotiated and what is actually requested becomes visible, provided you have the right tools to see it.

What to check on each invoice:

Do the invoiced prices correspond to the corresponding purchase order?

Do the invoiced quantities correspond to the quantities actually delivered (delivery note)?

Are the discounts mentioned on the purchase order correctly applied on the invoice?

Are the payment conditions (deadlines, any early payment discounts) in line with the contract?

Are there additional invoicing lines (fees, services) that were not anticipated?

This three-document reconciliation (purchase order, delivery note, invoice) is what accounting professionals call "3-way matching". It is the control standard, but it is still carried out manually in the vast majority of organisations.

Moving from occasional control to systematic control

Why manual control is no longer sufficient beyond a certain volume

Occasionally controlling a few strategic invoices is already good practice. But beyond a certain volume, meaning a few dozen invoices per month, several active suppliers and complex pricing conditions, manual control becomes a time sink.

An internal study conducted with ZYLIO clients shows that the manual processing of an anomaly on an invoice mobilises on average between 45 and 80 minutes of cumulated time (detection, verification, exchange with the supplier, correction, follow-up). Multiplied by the monthly volume of undetected anomalies, the human cost of manual control often exceeds the value of the discrepancies it allows to recover.

Manual control has another structural flaw: it is selective. You control the large invoices, the strategic suppliers, the periods of high activity. You let through small recurring discrepancies, secondary suppliers, busy end-of-month periods. It is precisely there that contract leakage thrives.

How to structure a regular control process

Systematic control does not require automating everything immediately. It first requires structuring the method, then identifying where automation brings the most value.

The 4 steps of a structured control process:

Centralise contractual conditions in a single, up-to-date reference document: one document per supplier that serves as the reference in case of discrepancy.

Define alert thresholds: below what discrepancy amount you accept the margin of error, above which you trigger a systematic verification.

Standardise exchanges with suppliers for correction requests: a clear process, defined deadlines, documented traceability.

Regularly measure the anomaly rate by supplier and by category: it is this monitoring that makes it possible to identify structurally problematic suppliers.

The role of automation: handling volume without burdening teams

The automation of document control answers a simple question: how to verify 500 invoices per month with the same rigour as a single one, without multiplying headcount?

An AI agent dedicated to contract leakage control is capable of automatically cross-referencing each invoice with the purchase order and the reference contractual conditions, detecting discrepancies line by line (prices, quantities, discounts, fees) and generating an anomaly report prioritised by amount and by supplier.

What used to take 3 hours of manual work for a complex invoice takes a few seconds. And above all, no invoice goes through without control, whether it is for €200 or €200,000.

What this represents concretely over 12 months

For an organisation with an annual procurement volume of 3 million euros and a contract leakage rate of 2%, in the low average of sector estimates, systematic control makes it possible to recover €60,000 in margin per year. Without renegotiation, without calling the supplier relationship into question, without new budgets.

Simply by applying what has already been negotiated.

What to remember

Contract leakage does not show up in your usual dashboards. It is only revealed when the right control checkpoints are put in place on the quote before any commitment, on the purchase order before execution and on the invoice before payment.

These three levels of control form a simple and actionable method. Structuring it takes time. Automating it allows it to be maintained over time, regardless of volume.

And for organisations that want to know precisely where their contract leakage lies before investing in a complete process, there is a direct way to find out: test the control on a real sample of documents.

Discover ZYLIO !